Step by step with

our credit builder loan

Borrow no-interest up to £2,400 while building your credit. Remember, other factors can affect your score.

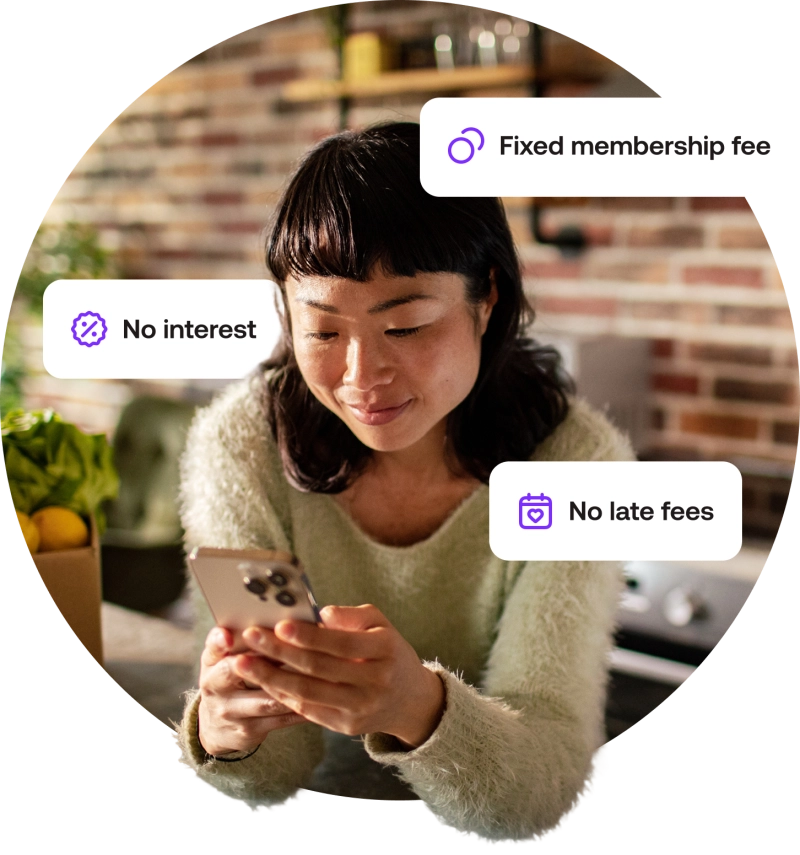

Borrowing made simple

Borrowing shouldn't feel complicated or risky. With Creditspring, you know exactly what you'll pay and when.

Credit that fits your life

Whether you're building credit or getting back on track, we have a plan that works for you.

The safer way to build your credit story

Get the credit support you need to stay in control and build confidence with every step.

Support every step of the way

Explore expert tips, learning resources, and financial tools that make money management simpler.

Real members. Real results.

Members love how clear, caring, and reliable our service feels — especially when life gets unpredictable.

Easy and straightforward. Nothing hidden, so nothing to worry about!

Rachel E Creditspring Member, 8 Oct 2025

Begin your credit journey

Checking has no impact on your credit score.

FAQs

Money stuff can get confusing — that’s why we’ve covered some of the key questions here. Still need answers? You’ll find more in our help centre.

We do things a bit differently. Instead of adding interest, we'd rather give you a no-interest loan and charge a membership fee that is spread over the course of your agreement. We believe this is a simpler and honest way of doing business. It also means that as a member, you know you'll never pay more than your monthly membership fee and what you borrowed. Read on here

- You must be over the age of 18

- Have a UK bank account older than 3 months

- Earn a minimum of £14,000 per year

- Have no recent CCJ, IVAs or bankruptcies

However, if you choose to borrow only one advance, and you do so at the earliest point permitted, repay each instalment in full and on time, and the agreement runs for a minimum term of 12 months, the APR would be 162.5%

It is important to note that we don't offer refunds on monthly fees if you decide not to borrow the maximum amount of credit available to you during your membership. As always, it is important to read all the terms of your agreement before taking up a product with us. Read on here

If you are eligible for a Creditspring membership and you accept a membership, our credit check will then be posted as a “hard footprint” on your credit report, accessible by other lenders. Once you are a member, we will continue to report your monthly membership payments and any repayments of your advances to the credit agencies.